WITH oil production poised to reach over 1.3 million barrels per day by 2030, Guyana will be positioned among the top 15 oil producers in the world, accounting for about one per cent of global production.

By 2035, exploration and development costs should be fully recovered, which means that the Government’s take will increase from 14.5% currently, to, conservatively, 25%, resulting in a projected increase to peak at approximately US$8 Billion annually thereafter from the Stabroek Block, all other things being equal.

The global demand for fossil fuel remains buoyant amidst an increasingly focused global agenda on the energy transition goals by 2050. Global demand is expected to remain strong, especially since the U.S needs to rebuild its strategic reserves, which currently only represents less than one month’s daily consumption.

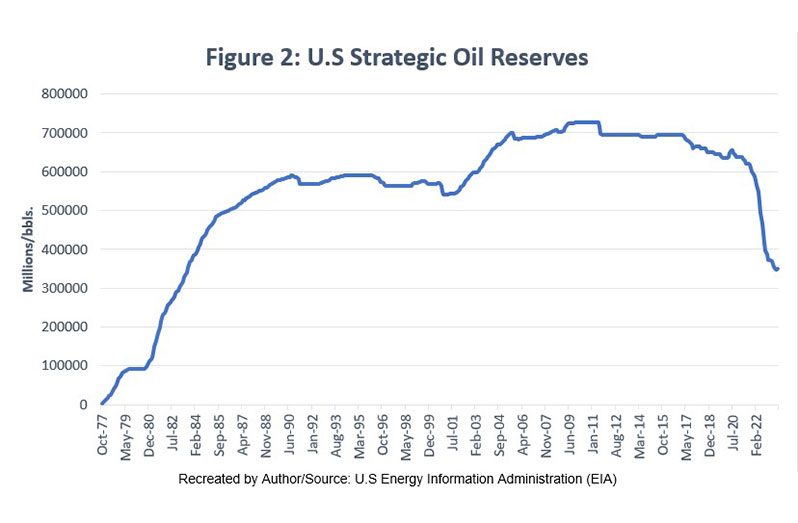

The U.S strategic reserves is down to its lowest level in decades at 347 million/bbls (2023) down from a peak level of 727 million/bbls in July 2011. Other countries such as India and China are also building up strategic reserves as part of their energy security strategy.

Therefore, owing to ExxonMobil Guyana’s unprecedented success rate in the Guyana’s Stabroek Block, Guyana’s increasing global importance in the energy landscape is cemented.

In the first year of production, the Government’s annual earnings averaged US$300 Million, which moved to about US$1 Billion based in 2022 and 2023. With the addition of a third FPSO, annual projected earnings is estimated to reach US$2.1 Billion at an average price of US$70 per barrel in FY 2024, all other things being equal.

ExxonMobil Guyana and their co-ventures (CoVs) are aiming to have 10 FPSOs online by 2030, producing an estimated 1.3 million/bpd, given the proven reserves to date of over 11 billion barrels oil equivalent.

DISCUSSION AND ANALYSIS

At this level of scaled production of 1.3 million/bbls by 2030, the Government’s annual earnings is an estimated US$4.7 Billion. By 2035, exploration and development costs should be fully recovered, which means that the Government’s take will increase from 14.5% currently, to, conservatively, 25%, resulting in a projected increase to peak at approximately US$8 Billion annually thereafter from the Stabroek Block.

Thus, with oil production poised to reach over 1.3 million barrels per day by 2030, Guyana will be positioned among the top 15 oil producers in the world, accounting for about 1% of global production.

It is worth noting that considering the size of the Stabroek Block, which is an estimated 26,806 km2,, to date, less than 2% was fully explored. This includes the 46 discoveries to date.

This means that by 2027 when the 2016 Prospecting License expires, not more than 3% of the Stabroek Block will have been fully explored, effectively placing the Government of Guyana in a position to repossess 97% of the Stabroek Block.

Consequently, the new fiscal terms, inter alia, the new model Production Sharing Agreements (PSAs) shall be applied to any new exploration and production licenses thereafter.

THE GLOBAL OIL INDUSTRY CONTEXT

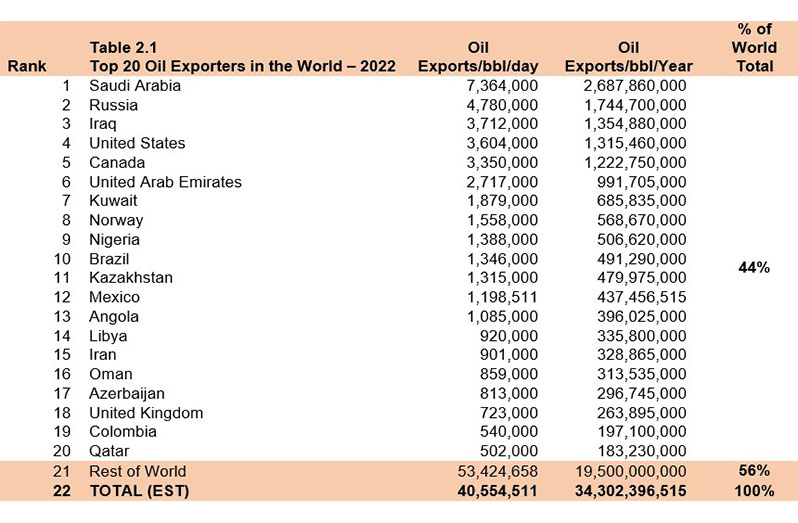

The top 10 countries that hold the largest proven oil reserves in the world account for 86.4% of the global proven reserves, while the rest of the world’s proven reserves account for 13.6. In 2022, the top 20 oil exporters accounted for 44% of global oil production, while the rest of the world accounted for 56%.

Saudi Arabia remained the largest oil producer in the world, accounting for 8% of global production. The second, third, fourth, and fifth largest producers are Russia, Iraq, the UAE, and Kuwait accounting for 5%, 4%, 3% and 2% of global production respectively.

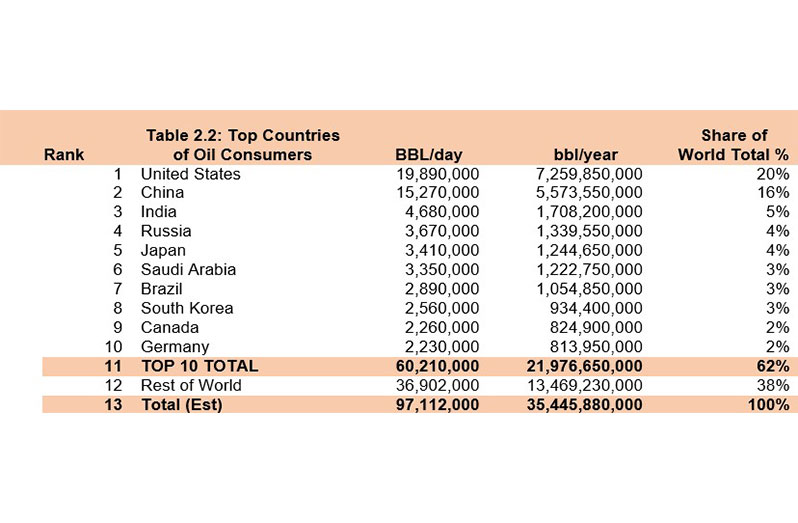

The top 10 largest consumers of oil accounted for 62% of global consumption of which the United States is the largest, accounting for 20% of global consumption, followed by China and India accounting for 16% and 5% of global consumption respectively

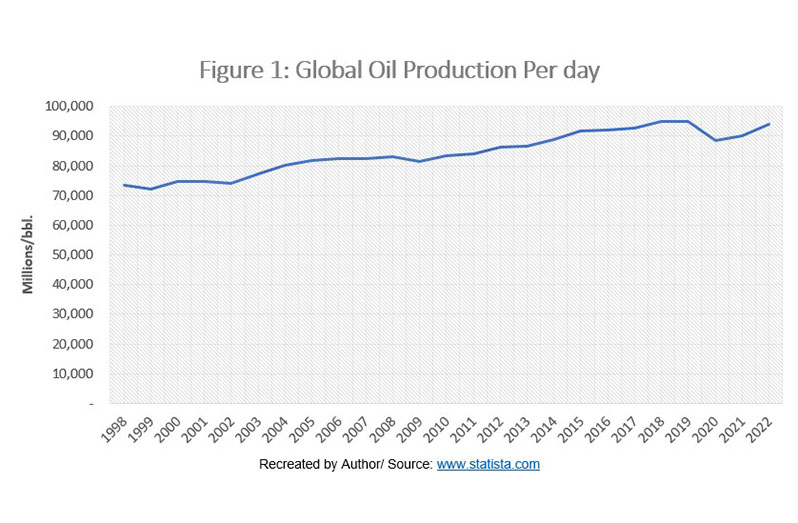

Global oil production has increased from 78.5 million bbls/day in 1998 to 93.9 million bbls/day in 2022, reflecting an increase of 20% cumulatively over the last 24 years (1998-2022), or an average of 0.83% annually for that period.

The United States strategic oil reserves fell to record low levels in July 2023 since July 1983, an almost forty (40) years’ record low level to 347.5 million bbls, down from a high of 718.2 million bbls in July 2011. This level of decline is a direct result of the Russia-Ukraine crisis, which saw oil prices soaring to historical peak levels since 2008-2014.

This prompted the U.S Government to dip into its reserves to stabilise oil prices in order to bring about some ease for the U.S consumers.

DRIVERS OF GLOBAL DEMAND, AND OUTLOOK

The global demand for fossil fuel remains strong amidst an increasingly focused global agenda on the energy transition goals by 2050. Global demand will continue to be strong, especially since the U.S needs to build up its strategic reserves, which currently only represents less than one month’s daily consumption.

Other countries such as India and China are also building up strategic reserves as part of their energy security strategy. With respect to the energy transition agenda, the world continues to lag behind on multiple fronts, such that it may ultimately render the 2050 goals unachievable. In this regard, there are a number of gaps to be bridged in order to reach net zero by 2050, as outlined hereunder.

The Generation Gap. In recent years, backed by subsidy schemes, tax credits, and a falling levelized cost of energy, the installation of renewable energy capacity has expanded tremendously. Globally, 1,282 gigawatts (GW) of renewable power capacity was added to the energy system between 2016 and 2021, and the International Energy Agency (IEA) projects that an additional 2,400 GW of renewable capacity will be installed in 2022 and 2027. However, if the world is to reach net zero by 2050, capacity will have to grow to more than 27,000 GW―an eightfold increase from 2021 levels.

The Grid Gap. Over the past decade, the world has invested an average of $300 billion per year. According to the IEA, annual investments will need to rise to the range of US$560 billion to US$780 billion in the 2030s.

The Storage Gap. Renewable energy tends to be intermittent (the sun doesn’t always shine, and the wind doesn’t always blow, while the demand for electricity is relatively constant and predictable). Hence, to have an orderly transition to a decarbonised grid, a significant amount of electricity storage capacity will be required, in the form of batteries or pumped hydropower schemes. Significant investments in grid-scale battery storage have been made.

In 2022, globally, 16 GW of grid-skill battery storage was added. According to the IEA, to get on track with the net-zero targets, which would require a 143-fold increase by 2050, annual additions must pick up significantly to an average of more than 80 GW per year over the 2022 to 2030 period.

The total funding gap needs to almost triple. To keep on track with net-zero emissions by 2050 goals, the IEA estimates that annual investment in clean energy will have to rise substantially from the projected 2023 level of US$1.8 trillion to US$4.6 trillion in 2030. With this in mind, bridging the energy transition gap is likely to remain a challenging task in meeting those targets to narrow the gap. Therefore, the global demand for fossil-fuel will continue to be strong for at least for the next 3 decades or another century.

The global demand for fossil fuel remains buoyant amidst an increasingly focused global agenda on the energy transition goals by 2050. Global demand is expected to remain strong, especially since the U.S needs to rebuild its strategic reserves, which currently only represents less than one month’s daily consumption.

The U.S strategic reserves is down to its lowest level in decades at 347 million/bbls (2023) down from a peak level of 727 million/bbls in July 2011. Other countries such as India and China are also building up strategic reserves as part of their energy security strategy.

Therefore, owing to ExxonMobil Guyana’s unprecedented success rate in the Guyana’s Stabroek Block, Guyana’s increasing global importance in the energy landscape is cemented.

Over the medium-term, Guyana is projected to experience sustained double-digit growth over the next decade with continued oil production and exploration, averaging about 28% annual GDP growth. Concurrently, the Government is pursuing an ambitious economic diversification, and transformative development agenda that was developed three decades ago.